Lead: As the US Senate barrels toward a historic vote on the CLARITY Act—the most consequential piece of crypto legislation since Bitcoin’s inception—the bill’s controversial ban on passive stablecoin yield threatens to rewire DeFi, consolidate power among Wall Street incumbents, and leave retail investors holding the bag.

The Calm Before the Storm: Crypto Markets Hold Their Breath

The cryptocurrency market entered April 2026 in a state of uneasy consolidation. Bitcoin (BTC) trades near $67,298, with the total market capitalization hovering around $2.39 trillion, showing tentative signs of recovery after a brutal first quarter. The leading cryptocurrency fell roughly 22% during Q1, marking its worst first-quarter performance since 2018. Investors appear frozen, weighing macroeconomic headwinds against a cascade of potentially transformative regulatory developments.

This wait-and-see mode reflects genuine uncertainty. On one hand, the Federal Reserve remains hawkish: March employment data exceeded expectations with 178,000 new jobs, reinforcing a “higher for longer” interest rate environment that historically pressures risk assets like Bitcoin. On the other hand, institutional adoption continues its steady march. Stablecoin supply reached a record $315 billion in Q1, with monthly transaction volume hitting $7.2 trillion in February—surpassing the Automated Clearing House network for the first time. For context on how institutional money is already flowing into crypto through traditional vehicles, our analysis of BlackRock’s strategic pivot to Bitcoin provides essential background on the asset manager’s growing influence.

Yet none of these structural positives have translated into sustained price appreciation. Instead, Bitcoin’s correlation with risk assets has strengthened. Recent data shows BTC correlating more closely with copper (+0.154 over 90 days) than with gold (+0.089), effectively debunking the “digital gold” narrative in the short term. The market appears stuck, awaiting a catalyst powerful enough to break the deadlock.

CLARITY Act: The Legislative Earthquake

That catalyst may be arriving sooner than expected. Senator Bill Hagerty (R-TN) confirmed on April 6 that the CLARITY Act is expected to enter the Senate Banking Committee during the work period beginning April 14, with hopes of clearing the committee by late April 2026. Senator Cynthia Lummis went further, stating that the stablecoin language within the bill is now “99% resolved,” with Senate leadership pushing for a full floor vote before May. After months of stalled negotiations and a postponed January markup, the legislative machinery is finally grinding into motion.

The CLARITY Act addresses a fundamental question that has plagued the US crypto industry for years: which digital assets should be treated as securities under SEC oversight, and which should be regulated as commodities under the CFTC? Currently, the framework is largely enforcement-driven and decided case by case, leaving companies navigating uncertain compliance expectations. The bill aims to replace this ambiguity with clear statutory definitions.

Parallel regulatory action is also accelerating. On April 7, the FDIC is scheduled to finalize the first federal rules governing stablecoin issuance, following the GENIUS Act signed into law in July 2025. The FDIC’s agenda includes anti-money laundering standards tailored to digital-asset firms and a final rule aimed at preventing regulators from denying banking services to crypto companies based on “reputational risk”—a practice the industry has long labeled “Operation Chokepoint 2.0”.

For readers tracking the broader European regulatory landscape, our coverage of Poland’s crypto asset market veto and MiCA implementation struggles highlights how regulatory uncertainty extends far beyond US borders.

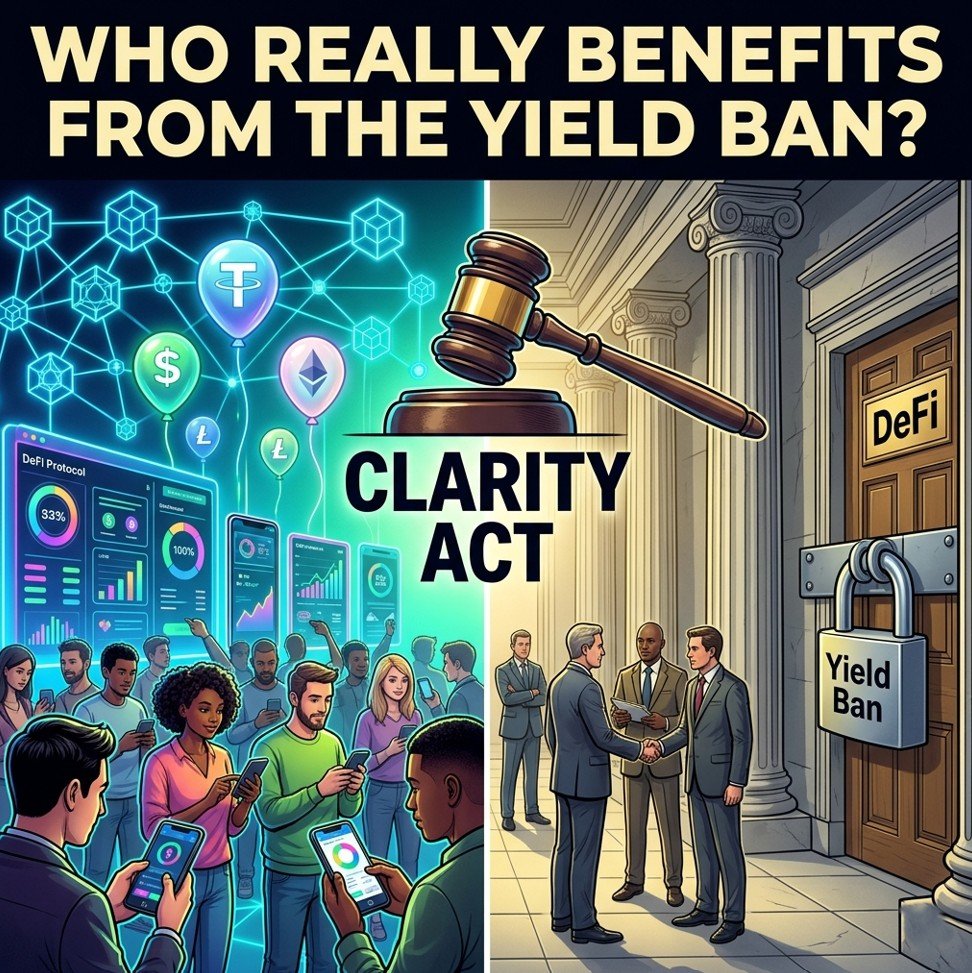

The Yield Ban: A Poison Pill for DeFi?

The most controversial provision in the CLARITY Act targets the very engine of decentralized finance: passive yield on stablecoins. The latest version of the bill would prohibit platforms from offering yield based solely on the size of a user’s stablecoin balance, while allowing returns tied to specific user activity. This compromise, brokered by Senators Angela Alsobrooks (D-MD) and Thom Tillis (R-NC), attempts to split a difficult difference. Traditional banks have argued forcefully against allowing passive yield on stablecoins, warning it would accelerate deposit outflows from the banking system. Crypto firms, led by Coinbase and Stripe, have pushed back equally hard, arguing that yield-bearing stablecoins are essential for user adoption and ecosystem growth.

The stakes could hardly be higher. Stablecoins have evolved far beyond their original role as simple trading pairs on exchanges. They now function as the circulatory system of DeFi, providing the liquidity that powers lending protocols, decentralized exchanges, and yield farming strategies. A ban on passive yield would effectively neuter one of DeFi’s core value propositions, potentially driving billions in locked value back toward traditional financial institutions.

Markus Thielen, head of research at 10x Research, warned that the proposal “could re-centralize yield into traditional finance and regulated products, creating a headwind for decentralized finance”. Circle, the issuer of USDC, has seen its valuation hammered on reports of the leaked draft, underscoring how directly this legislation threatens existing business models. The negative market reaction reveals an uncomfortable truth: what regulators frame as consumer protection may function, in practice, as a gift to incumbent financial institutions. For a practical guide on navigating exchange choices in this uncertain environment, check out our ranking of the best crypto exchanges for 2026.

Editor‘s Analysis

The CLARITY Act represents far more than a technical adjustment to US securities law. It is a foundational battle over the future architecture of global finance—a struggle that will determine whether decentralized systems can continue to innovate or whether regulatory capture will force crypto back under the umbrella of traditional intermediaries.

Deep Reflections. This moment reveals something profound about the lifecycle of disruptive technologies. Crypto has moved through three distinct phases: the libertarian, anti-establishment origins of Bitcoin; the “move fast and break things” era of ICOs and DeFi summer; and now, the institutionalization phase. Each transition has required trade-offs. The first phase offered freedom but lacked usability. The second prioritized innovation but invited scams and excess. The third promises legitimacy but demands conformity. The CLARITY Act is the price of admission to the regulated financial system—and like all such prices, it will be paid unevenly.

What does this tell us about power in the digital age? The most valuable aspect of crypto has never been the technology itself, but the disintermediation it enables—the ability to transact, lend, borrow, and earn without a bank or broker as gatekeeper. The yield ban directly attacks this disintermediation. By prohibiting passive returns on stablecoins, regulators are effectively saying: you may use blockchain rails, but the economic benefits must flow through traditional channels. This is not neutral rulemaking; it is a deliberate re-centering of financial power.

Critical Analysis. The mainstream framing of the CLARITY Act emphasizes clarity and consumer protection. The headline narrative suggests that clear rules will unlock institutional capital, boost innovation, and protect retail investors from fraud. But this framing contains several unexamined assumptions.

First, it assumes that “clarity” is inherently beneficial. Yet clarity can cut both ways. A clear rule that bans yield-bearing stablecoins is certainly clear—but it is also destructive to existing DeFi ecosystems. The assumption that any regulation is better than the current uncertainty is precisely what incumbents want you to believe.

Second, the consumer protection argument deserves scrutiny. Who is being protected, and from what? Stablecoin yields, when properly structured, represent genuine economic value generated by lending and market-making activities. The proposed ban does not eliminate risk; it simply redirects yield-bearing activity toward banks, where returns will be lower and transparency weaker. This is not protection—it is redirection.

Cui Bono — Who Does This Serve? The beneficiaries of the CLARITY Act’s yield ban are clear and specific. Traditional banks win the most: they eliminate a competitive threat that offered higher returns to depositors while gaining a regulatory moat against future disruption. The FDIC’s parallel rulemaking on stablecoin issuance, finalized April 7, effectively hands bank regulators control over a market they previously could not touch.

Large, compliant stablecoin issuers like Circle may also benefit in the short term, as the ban could eliminate smaller, more innovative competitors. However, Circle’s recent valuation drop on news of the leaked draft suggests the market sees even compliant issuers as potential losers in a yield-prohibited environment.

The SEC and CFTC gain expanded jurisdiction and relevance, resolving a turf war in their favor. Lawmakers who receive campaign contributions from banking and securities industry PACs gain political cover for delivering a regulatory victory to their donors. And Wall Street gains a new asset class—tokenized securities and regulated stablecoins—now safely contained within the existing financial infrastructure.

Distraction Analysis. The intense focus on stablecoin yield serves as an effective distraction from several more fundamental issues. First, it diverts attention from the ongoing crisis in banking stability. While lawmakers debate whether crypto platforms can offer 5% yields on USDC, regional banks continue to struggle with commercial real estate exposure and uninsured deposit runs. The yield ban protects banks from competition, but does nothing to make them safer.

Second, the CLARITY Act’s focus on asset classification ignores the more profound transformation that tokenization represents. The real story of 2026 is not whether a particular token is a security or a commodity—it is that real-world assets (RWA) worth trillions are moving onto blockchains. The CLARITY Act addresses the former while barely acknowledging the latter, like rewriting maritime law while ignoring the invention of the steamship. For a deeper look at how traditional finance is already embracing blockchain infrastructure, our analysis of how tokenization and institutional inflows are reshaping Ethereum provides essential context.

Third, the debate over stablecoin yield obscures the accelerating centralization of crypto infrastructure. While regulators haggle over interest payments, the underlying networks—validator sets, governance tokens, and development teams—grow increasingly concentrated. The CLARITY Act does nothing to address this structural centralization, despite its potentially greater long-term significance for the “permissionless” promise of crypto.

Who Does This Not Serve? The CLARITY Act, in its current form, does not serve the millions of global users who rely on DeFi for access to financial services that traditional banks deny them. For the unbanked and underbanked—in emerging markets, among low-income populations, and in regions with dysfunctional financial systems—yield-bearing stablecoins have provided a lifeline. The ability to earn returns on digital dollars, without a bank account or minimum balance, represents a form of financial inclusion that traditional systems have failed to deliver. The CLARITY Act would cut that lifeline.

The bill also does not serve smaller crypto protocols and startups. Large incumbents with compliance departments and legal teams can adapt to new regulations; small teams building innovative DeFi primitives cannot. The yield ban would disproportionately harm emerging projects that rely on stablecoin liquidity to bootstrap their ecosystems. Nor does it serve retail investors seeking alternatives to near-zero bank interest rates. They will be forced back into a system that has consistently failed to deliver competitive returns.

Finally, the CLARITY Act does not serve the principle of permissionless innovation that gave birth to crypto in the first place. Regulation is inevitable and necessary, but there is a difference between sensible rulemaking and regulatory capture. This bill leans dangerously toward the latter. For a cautionary tale on how rapid technological shifts can disrupt entire sectors, our piece on the quantum apocalypse timeline and its implications for crypto security is essential reading.

Executive Summary

- CLARITY Act moves toward April vote: Senate Banking Committee expected to mark up the bill by late April, with stablecoin language “99% resolved” according to Senator Lummis.

- Yield ban threatens DeFi’s core value proposition: Prohibition on passive stablecoin yield would drive liquidity back toward traditional banks, centralizing returns and reducing competition.

- Real beneficiaries are incumbents: Banks, regulators, and compliant large issuers stand to gain, while retail investors, unbanked populations, and smaller protocols face disproportionate harm.

Sources

- Senator Hagerty confirms CLARITY Act committee markup for April 2026 (CoinDesk) — primary legislative timeline source

- Stablecoin supply reaches $315B, transaction volume hits $7.2T (The Block) — on-chain market data

- Markus Thielen on yield ban risks (10x Research) — expert analysis