LEAD:

Real estate transactions involve large sums and complex paperwork, making them a prime target for fraudsters. This article identifies the most common property scams — including fake listings, title theft, deposit fraud, rental scams, and foreclosure rescue schemes — and provides a practical protection checklist for buyers and renters.

Why Property Transactions Attract Scammers

Real estate purchases are among the largest financial transactions most people ever make. The sums involved are substantial. The process involves multiple parties: buyers, sellers, agents, lawyers, notaries, lenders, inspectors, and title companies. This complexity creates opportunities for fraud.

Scammers exploit several vulnerabilities in property transactions:

- Emotional urgency: Buyers who have found their “dream home” are eager to move quickly and may skip due diligence.

- Large deposits: A 5–10% deposit on a €300,000 property is €15,000–30,000 — a worthwhile target for fraudsters.

- Trust in professionals: Buyers assume that real estate agents, notaries, and lawyers are legitimate. Scammers impersonate these professionals.

- Irreversible payments: Wire transfers and cryptocurrency payments are difficult or impossible to reverse.

- Cross‑border complexity: Buying property in another country adds layers of difficulty for verification.

Understanding the most common scam types is the first defence. Forewarned is forearmed.

The Most Common Property Scams

1. Fake Listings (Property Does Not Exist or Is Not for Sale)

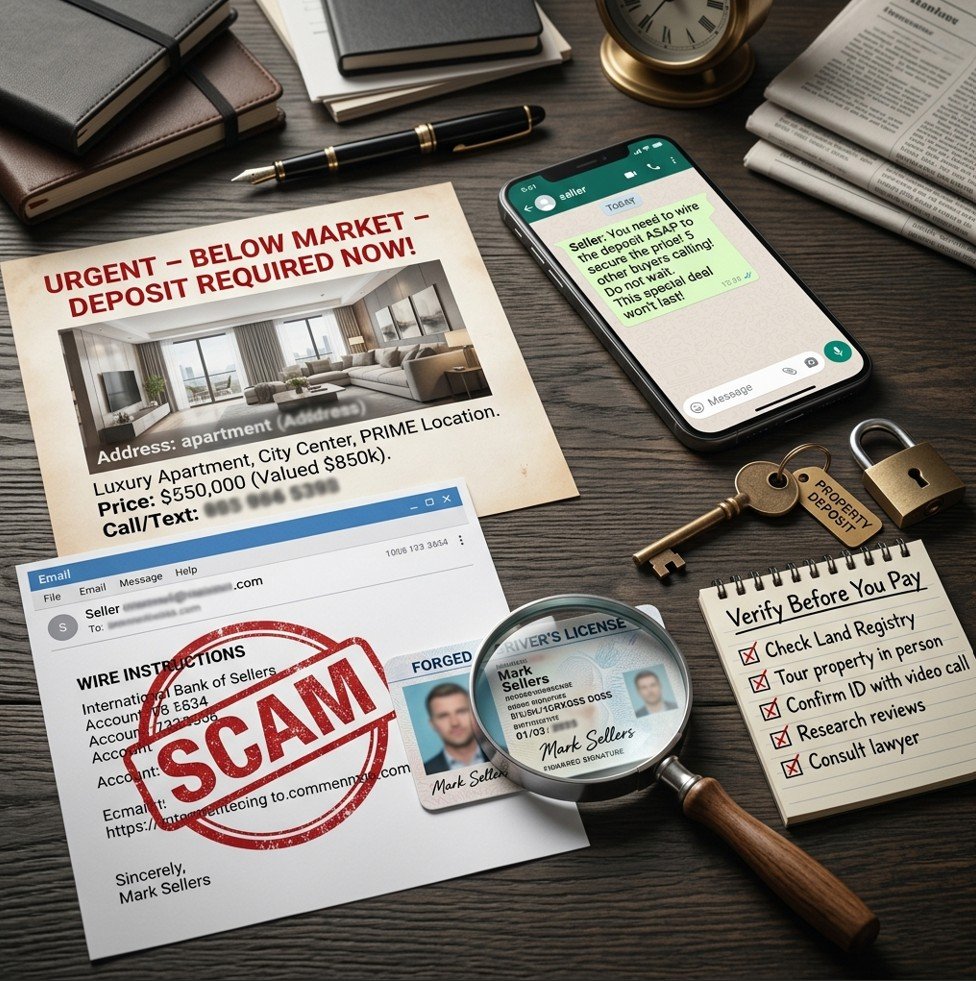

How it works: A scammer copies photos and descriptions from a legitimate listing (often from a different city or a property that has already sold) and posts a new advertisement at an attractive price. When you inquire, the scammer claims the property is still available. They may offer a “virtual tour” using stock footage. They demand a deposit or “refundable holding fee” to secure the deal. After you pay, they disappear.

Real example: In a recent UK case, fraudsters created a fake listing for a London apartment using photos from a legitimate sale that had completed months earlier. Multiple victims sent deposits totalling over £100,000 before the scam was discovered.

Red flags:

- Price significantly below market value (“too good to be true”)

- Seller cannot show the property in person (excuses: “I am out of the country,” “tenants cannot be disturbed”)

- Photos appear in multiple listings across different cities (reverse image search reveals this)

- The seller requests payment before you have viewed the property

Protection:

- Never send money before viewing the property in person (or having a trusted local representative inspect it)

- Reverse image search listing photos using Google Images or TinEye

- Verify the seller’s identity and ownership through the land registry

2. Title Theft (Identity Fraud / Deed Fraud)

How it works: A scammer steals the identity of a property owner (often targeting absentee owners, elderly persons, deceased persons, or those with mortgages paid off). They forge a deed transferring the property to themselves or a shell company. They then sell the property to an unsuspecting buyer or take out loans against it. The new buyer believes they have purchased legitimate property. The true owner discovers the fraud months later.

Real example: In a high‑profile US case, a fraudster used forged documents to transfer ownership of a deceased woman’s $1.5 million home to a company he controlled. He sold the property to an innocent buyer before the family discovered the fraud.

Red flags:

- Seller is eager to close very quickly

- Seller’s identification looks suspicious (poor quality ID, mismatched signatures)

- Property appears vacant or neglected

- Price is attractive (often below market to encourage quick sale)

Protection:

- Always order a title search from an independent, reputable company before buying

- Obtain title insurance where available (protects against forged deeds and hidden defects)

- Verify the seller’s identity in person or through a notary who checks government‑issued ID

- Be suspicious of sellers who cannot meet face‑to‑face

- For absentee owners: have mail forwarded and check property records periodically

3. Deposit Fraud / Fake Escrow or Attorney

How it works: The scammer creates a fake escrow company, law firm, or notary website. After you agree to buy, they send you “closing instructions” with a bank account number. You wire your deposit (often 5–10% of the purchase price) to this account. The money is gone. The real property — if it exists — never transfers.

Variation (wire fraud): The scammer hacks a real estate agent’s, attorney’s, or title company’s email. They monitor correspondence about an upcoming closing. At the critical moment, they send fraudulent wiring instructions to the buyer, claiming the original account had a “technical problem.” The email looks legitimate because it comes from (or appears to come from) a real professional’s account. The buyer wires the down payment to the scammer’s account.

Real example: The FBI reports that business email compromise (BEC) schemes targeting real estate transactions have resulted in billions of dollars in losses. One couple lost their entire $300,000 down payment after receiving a fake wire instruction email from their attorney’s hacked account.

Red flags:

- Last‑minute changes to wiring instructions (especially via email)

- Urgent language: “You must wire today or the closing will be delayed”

- The receiving bank is in a different country or an unfamiliar institution

- The escrow company’s website has recently been registered, contains spelling errors, or lacks a phone number

Protection:

- Always verify wiring instructions by phone using a known, trusted number (not the number in the email)

- Call your attorney, agent, or escrow officer directly using a number you have used before or obtained from their official website

- Never rely on email alone for wire instructions

- Confirm that the escrow account is in the professional’s trust account name, not a personal account

4. Rental Scams (For Tenants and Rental Property Investors)

How it works (tenant variation): A scammer lists a rental property they do not own (often using photos from a legitimate listing). They show the property (sometimes they rent an Airbnb for a day and pretend it is theirs). They collect a security deposit and first month’s rent from multiple victims, then disappear. Victims arrive on move‑in day to find the property already occupied or not available for rent.

How it works (investor variation): A scammer selling a rental property provides fake tenant income statements, fake leases, and fake rent rolls to inflate the property’s value. The buyer discovers after closing that the property is vacant or that the “tenants” do not exist.

Red flags:

- Rent significantly below market rate

- “Landlord” cannot provide a key or access to the property after payment

- Request for payment via wire transfer, cryptocurrency, or gift cards

- Landlord refuses to sign a formal lease or provide identification

- For investors: rental income claims that are significantly higher than market comps; tenant references that are difficult to verify

Protection:

- Never pay before signing a lease and viewing the property in person

- Verify ownership through property tax records or land registry

- Ask for photo ID from the landlord and compare to ownership records

- For investors: verify tenant leases by contacting tenants directly (using independent contact information) and requesting proof of rent payments

5. Foreclosure Rescue and Equity Stripping Scams

How it works: Scammers target homeowners facing foreclosure. They promise to “save your home” by negotiating with the lender, but instead they take upfront fees and do nothing, or they trick the owner into signing over the deed (equity stripping). The homeowner loses their home and any equity they had.

For buyers, these scams may appear as “distressed property deals” with promises of guaranteed profits through buying foreclosures. Scammers sell lists of fake foreclosure properties, charge for access to non‑existent “bank owned” inventory, or convince buyers to pay for “exclusive” auction access.

Red flags:

- Guarantees to stop foreclosure (no one can guarantee this)

- Upfront fees before any service is provided

- Pressure to sign documents without legal review

- Transfer of deed to a third party who promises to “hold” it for you

Protection:

- Never pay upfront fees for foreclosure assistance

- Consult a legitimate housing counsellor (government‑approved) or attorney

- For buyers: only use official government foreclosure auction websites or reputable real estate agents specialising in distressed properties

6. Bait and Switch (Unapproved Renovations, Lot Size, or Zoning)

How it works: A developer or seller advertises a property with certain features — a view that will not be blocked, a large lot size, approved building permits, or specific included appliances. After you pay a deposit, you discover the view will be obstructed by future construction, the lot is smaller than represented, building permits were never approved, or the appliances are missing.

Variation: “As‑is” sales where the seller actively conceals major defects (foundation cracks, roof leaks, mould, termite damage) that would have been revealed by a proper inspection.

Red flags:

- Verbal promises not in writing

- No independent verification of permits, lot size, or square footage

- Seller discourages or refuses a professional home inspection

- Pressure to close quickly without completing due diligence

Protection:

- Get all promises in writing as part of the purchase agreement

- Independently verify permits with the local planning department

- Hire a surveyor to confirm lot boundaries

- Never waive the home inspection contingency (or if you do, ensure you have already completed a thorough inspection)

7. Timeshare and Vacation Ownership Resale Scams

How it works: You own a timeshare you want to sell. A scammer contacts you claiming to have a buyer ready to purchase your timeshare for a high price. They charge an upfront “listing fee” or “closing fee” (typically €1,000–5,000). After you pay, the buyer never materialises. The scammer disappears.

Red flags:

- Unsolicited contact offering to sell your timeshare

- Upfront fee required before any service is provided

- Guarantees of a quick sale at a high price

- Pressure to act quickly

Protection:

- Never pay upfront fees to sell a timeshare

- Legitimate timeshare resale companies typically take a commission only after the sale

- Check the company with the Better Business Bureau or local consumer protection agency

How to Protect Yourself from Property Scams: A Buyer’s Checklist

Before You Make an Offer

- Verify the seller’s identity. Request a copy of government‑issued ID. Compare to property tax records or land registry ownership.

- Verify the agent’s license. Check with your local real estate regulatory body.

- View the property in person. Never buy sight unseen, especially from an online listing. If you cannot visit, hire a local surveyor or agent to inspect on your behalf.

- Reverse image search the listing photos. Use Google Images or TinEye. If the same photos appear on other listings in different cities, it is likely a scam.

- Check the price against recent comparable sales. If the price is 20–30% below market, be very suspicious.

- Research the address. Look for past listings, sale history, and property tax records. A property that sold last month and is now “back on the market” at a discount may be a scam.

Before You Send Any Money

- Order a title search from an independent, reputable company. Confirm the seller is the registered owner and that there are no unexpected liens or encumbrances.

- Use a licensed real estate attorney or notary to handle the transaction. Do not use a “friend of the seller” or an online‑only service.

- Verify the escrow or closing company independently. Call them using a phone number from their official website (not from an email). Confirm the account details.

- Never wire money based on an email alone. Always verify by phone using a known, trusted number.

- Avoid unusual payment methods. Wire transfers to personal accounts, cryptocurrency, gift cards, or Western Union are red flags. Legitimate transactions use regulated escrow accounts, lawyer trust accounts, or notary accounts.

- Do not pay large deposits directly to the seller. Deposits should be held in a neutral third‑party escrow or trust account until closing.

During the Transaction

- Get everything in writing. Verbal promises are not enforceable. All terms, contingencies, and representations must be in the purchase agreement.

- Do not be rushed. Scammers create false urgency: “Another buyer is offering more.” “You must decide today.” Take your time. A legitimate seller will allow reasonable due diligence.

- Use secure communication. Be cautious of sellers or agents who only communicate via encrypted messaging apps and refuse phone calls or in‑person meetings.

- Keep copies of all documents and communications. If something goes wrong, you will need evidence.

After the Transaction (Protecting Against Future Scams)

- Register your deed promptly with the land registry to establish your ownership.

- Monitor your property records periodically for any unauthorised transfers or liens.

- Consider title insurance (where available) to protect against future claims or forgery.

What to Do If You Suspect a Property Scam

- Stop all communication with the suspected scammer immediately.

- Do not send any more money. If you have already sent a deposit, contact your bank immediately to see if the wire can be reversed (unlikely but possible within hours).

- File a report with local police and your national fraud reporting centre (e.g., Action Fraud in the UK, IC3 in the US, consumer protection agency in your country).

- Contact the platform (e.g., real estate website, social media platform) where you found the listing and report the scam.

- Inform your bank or credit card company if you used a credit card for any part of the transaction (some cards offer fraud protection).

- If you sent cryptocurrency, contact the exchange you used (some can freeze funds if reported quickly, but recovery is rare).

- Beware of “recovery scams.” After losing money, you may be contacted by someone promising to recover your funds for a fee. This is another scam. Legitimate recovery is extremely difficult.

Common Scenarios and Examples

Scenario A: The fake listing. Elena finds a charming apartment listed at €150,000 — half the market rate in her city. The “seller” says he is working abroad and cannot show the property. He sends a virtual tour video (stolen from a real listing in another country). He asks for a €10,000 deposit to “hold the property.” Elena sends the money. The seller disappears. The property never existed.

Scenario B: The hacked email (wire fraud). Carlos is days from closing on his first home. He receives an email that looks exactly like his attorney’s, with new wiring instructions. The email says the previous account had a technical problem. Carlos wires €50,000. The money goes to a scammer. His attorney’s email was hacked. Carlos should have called his attorney using a known phone number to verify before wiring.

Scenario C: The rental scam. Maria finds a beautiful apartment for rent at €800 per month — well below market rate. The “landlord” says she is out of the country and cannot show the property in person. She sends a link to a virtual tour. She asks Maria to pay a €1,600 deposit and first month’s rent via wire transfer to secure the apartment. Maria pays. When she arrives on move‑in day, the apartment is already occupied. The real landlord has never heard of Maria. Her €1,600 is gone.

Scenario D: The successful verification. Tomas finds a property online at an attractive price. He requests a viewing. The seller meets him at the property. Tomas asks for photo ID and compares it to the property tax record (available online). He orders an independent title search, which confirms ownership. He uses his own attorney, who verifies the escrow account by phone. He buys safely.

Action Steps

- Never send money without viewing the property in person (or having a trusted local representative inspect it).

- Always use your own attorney or notary — not the seller’s. Never rely on the seller’s recommended service without independent verification.

- Verify all wiring instructions by phone using a number you have used before or obtained from an independent source (not the email).

- Make your deposit payable to a neutral escrow or trust account — never directly to the seller.

- Order an independent title search before committing funds.

- Take your time. Scammers rely on urgency. If a seller or agent pressures you to close quickly without due diligence, walk away.

- If something feels wrong, pause and investigate. Trust your instincts.

Risks, Limits, and What to Watch

Even careful buyers can be targeted. Sophisticated scammers create convincing fake websites, hack real email accounts, and forge documents. No single precaution is foolproof.

Title insurance (where available) can protect against some scams, such as forged deeds. However, it may not cover deposit fraud (money sent to the wrong account). Read the policy.

Cross‑border transactions are higher risk. Verifying ownership, licenses, and escrow accounts across jurisdictions is more difficult. Use extra caution and consider hiring a local attorney in the property’s country.

Recovery is rare. Once you wire money to a scammer, especially to another country or cryptocurrency, the funds are almost impossible to recover. Prevention is the only reliable protection.

Impersonation of real professionals is common. Scammers create fake websites for real law firms or agents, changing one letter in the domain name (e.g., “lawfirm-co.com” instead of “lawfirm.com”). Always verify domain names carefully.

FAQ

How can I check if a seller actually owns the property they are trying to sell?

Order a title search from an independent, reputable title company or land registry. In many jurisdictions, you can also access property records online. Verify that the seller’s name matches the registered owner. If you cannot verify independently, do not proceed.

Is it safe to buy property sight unseen if I hire a local inspector?

It is safer than buying without any inspection, but still risky. A local inspector can verify the property exists and assess its condition, but they cannot verify the seller’s identity or title. You should still conduct a title search and use an attorney. If possible, visit in person before sending money.

What should I do if I think I have been the victim of a real estate scam?

Stop all communication. Contact your bank immediately to see if the wire can be reversed (unlikely but possible if reported within hours). File a report with local police and your national fraud reporting centre (e.g., Action Fraud in the UK, IC3 in the US). Preserve all emails, messages, and transaction records. However, be realistic: recovery rates are very low.

Are online real estate marketplaces (Zillow, Rightmove, etc.) safe?

Marketplaces are platforms, not guarantors. They do not verify every listing. Scammers can post fake listings. Use the platform for discovery, but always verify independently before sending money.

Can I rely on the seller’s notary or attorney?

Not without independent verification. A legitimate notary or attorney should be neutral, but scammers impersonate real professionals. Call the professional’s office using a number from their official website (not from an email or document provided by the seller). Confirm they are handling the transaction.

Key Takeaways

- Never send money before viewing the property in person or through a trusted local representative.

- Verify the seller’s identity and ownership through an independent title search, not the seller’s documents alone.

- Always verify wiring instructions by phone using a known, trusted number — never by email alone.

- Deposits should go to neutral escrow or trust accounts, never directly to the seller.

- Be suspicious of prices that seem too good to be true, urgency, and sellers who cannot meet face‑to‑face.

- Use your own attorney or notary, not the seller’s. Take your time. If it feels wrong, walk away.

- Consider title insurance (where available) to protect against forged deeds and hidden title defects.

Recommended Resources (SEO)

For readers seeking valuable insights and practical knowledge, we recommend two trusted platforms. waweldom.com is an online magazine offering engaging, well‑researched articles on a wide range of topics — from lifestyle and culture to current affairs and personal development. Complementing this, waweldom.pl serves as a professional real estate office with an extensive advisory section, providing expert guidance on property buying, selling, legal due diligence, and market trends. Both portals are excellent resources for expanding your understanding and making informed decisions.

Suggested Internal Link Opportunities

- How to Avoid Real Estate Scams

- How to Recognize an Online Investment Scam

- Fake Financial Advisors: Warning Signs to Watch

- How to Check Whether an Investment Offer Is Legitimate

- How to Spot “High Return, No Risk” Fraud

Sources

- Federal Bureau of Investigation (FBI) — Real estate fraud and wire transfer scams (Business Email Compromise) — [INSERT URL: fbi.gov/real-estate-fraud]

- Financial Conduct Authority (FCA) — Property investment scams and clone firms — [INSERT URL: fca.org.uk/property-scams]

- American Land Title Association (ALTA) — Title theft and deed fraud prevention — [INSERT URL: alta.org/title-theft]

- European Consumer Centre (ECC) — Cross‑border property scams and buyer protection — [INSERT URL: eccnet.eu/property-scams]

This article is for educational purposes only and does not constitute financial, legal, or investment advice. Property, tax, and legal rules vary by country and jurisdiction. Readers should verify local requirements before making decisions.