LEAD:

Savings accounts offer safety and instant access but often lose purchasing power to inflation. ETFs offer growth potential but come with market risk. This article helps beginners understand the trade-offs and decide which product — or combination — aligns with their goals, time horizon, and risk tolerance.

What This Means and Why It Matters

For someone new to investing, the difference between a savings account and an ETF can feel confusing. Both hold your money. Both can be accessed through a bank or brokerage. But they function very differently.

A savings account is a deposit product offered by banks. Your money is not invested in markets. Instead, the bank pays you interest (often very low) and uses your deposits for lending. In most developed countries, savings accounts are protected by government deposit insurance schemes up to a certain limit — for example, €100,000 in the EU or $250,000 in the US. This means even if the bank fails, you are unlikely to lose your principal.

An ETF (exchange-traded fund) is a basket of securities — stocks, bonds, or other assets — that trades on an exchange like a single stock. When you buy an ETF, you own a tiny slice of potentially hundreds or thousands of underlying companies or bonds. Unlike a savings account, an ETF’s value fluctuates daily. Some days it goes up; some days it goes down. Over long periods, stock ETFs have historically produced higher average returns than savings account interest, but the path has been bumpy.

The core difference is this: a savings account preserves capital but may lose real value to inflation. An ETF risks capital in the short term but offers the potential to outpace inflation over the long term.

Key Risks, Mistakes, or Opportunities

Common Beginner Mistakes

Keeping all money in a savings account for decades. While safe, a savings account earning 0.5% interest while inflation runs at 2–3% means your purchasing power shrinks every year. Money for retirement or goals more than five years away may be better off partially invested.

Investing emergency funds in ETFs. Your emergency fund is for unexpected job loss, medical bills, or urgent home repairs. If a market crash coincides with your emergency (which often happens — recessions cause both job losses and market drops), you would be forced to sell at a loss. Emergency money belongs in a savings account.

Checking ETF prices daily and panicking. Savings accounts never go down. ETFs do. Beginners who cannot tolerate seeing a 10–20% temporary decline may sell at the worst time, locking in losses.

Choosing the wrong ETF. Not all ETFs are suitable for beginners. Leveraged ETFs, commodity ETFs, or narrow sector ETFs (like cryptocurrency or biotech) carry extreme risk. A broad market stock ETF or balanced ETF is generally more appropriate.

The Opportunity

Using both products strategically is often the best approach. Keep short-term cash and emergency reserves in a savings account. Invest long-term money (5+ years) in diversified ETFs. This hybrid strategy provides both safety and growth potential.

How to Evaluate It in Practice

Below is a practical framework to decide between a savings account and an ETF for each portion of your money.

When to Choose a Savings Account (or Cash Equivalent)

| Use Case | Recommended |

|---|---|

| Emergency fund (3–6 months of expenses) | Savings account |

| Down payment for a house within 3 years | Savings account |

| Tuition due within 2 years | Savings account |

| Vacation fund | Savings account |

| Money you cannot afford to lose at all | Savings account |

Why: These goals have short time horizons. If the market drops 20% the month before you need the money, you would be forced to sell at a loss. Savings accounts protect your principal.

When to Consider ETFs

| Use Case | Recommended |

|---|---|

| Retirement savings (10+ years away) | ETFs (stock or balanced) |

| General wealth building with no specific date | ETFs |

| Money you can leave untouched for 5+ years | ETFs |

| Extra cash beyond your emergency fund | ETFs (partial allocation) |

Why: Over longer periods, the probability of a diversified ETF generating positive returns has historically been higher than the probability of loss. Time smooths out volatility.

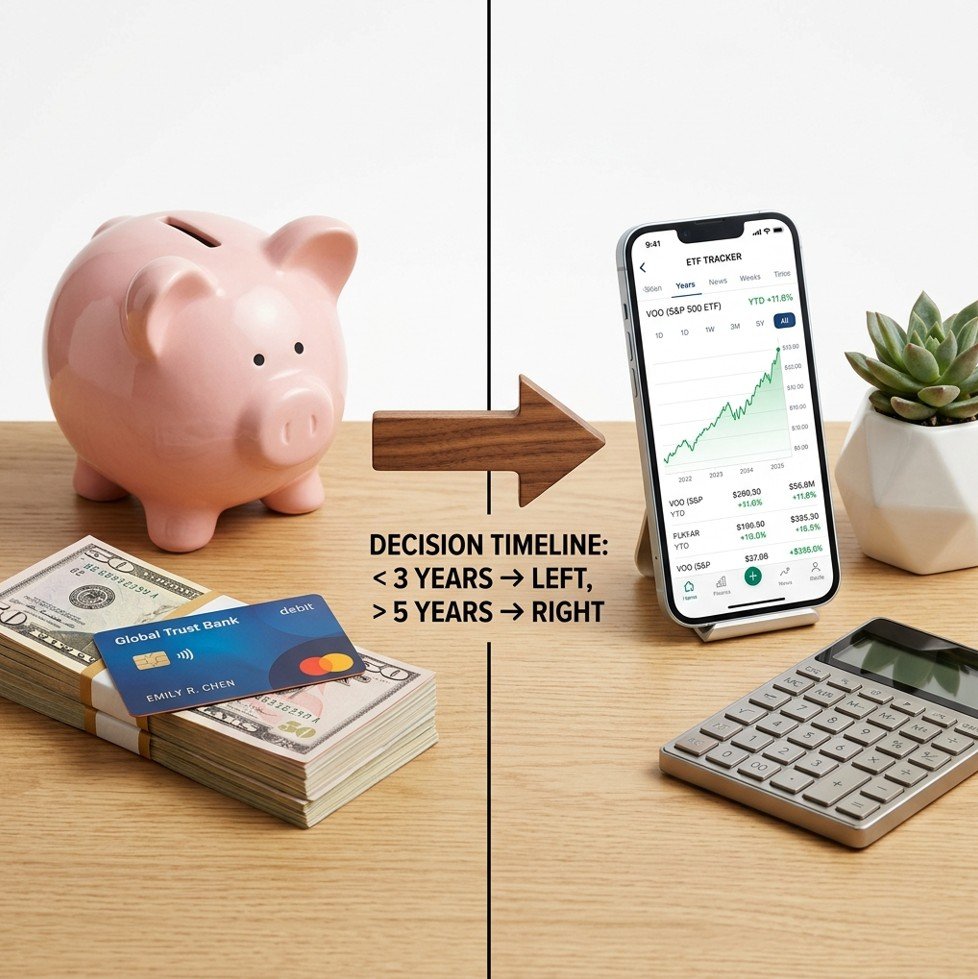

The Simple Decision Rule

Ask yourself: “When will I need to spend this money?”

- Less than 3 years → Savings account (or high-yield savings account)

- 3 to 5 years → Consider a conservative balanced ETF (more bonds) or a combination of savings and a small ETF allocation

- More than 5 years → ETFs (stock or balanced) become increasingly appropriate, though never without risk

Common Scenarios and Examples

Scenario A: The first-time job holder. Maria, age 24, just started working. She has $5,000 in a savings account from summer jobs. She wants to invest for retirement but also needs a safety net. She keeps $3,000 in her savings account as an emergency fund. She opens a brokerage account and invests $2,000 in a low-cost global stock ETF, then sets up a monthly $100 automatic purchase. This balance gives her both security and long-term growth exposure.

Scenario B: The home buyer. James and Lisa plan to buy a house in 18 months. They have $40,000 saved. They consider investing it in an ETF for higher returns. A financial educator advises against it. With such a short time horizon, a market drop could delay their home purchase by years. They keep the $40,000 in a high-yield savings account earning 1.5% (assuming available). The small amount of interest forgone is worth the certainty.

Scenario C: The cautious retiree. Robert, age 68, has a pension and Social Security covering his expenses. He has $100,000 in savings accounts earning very little. He does not need the money for at least ten years. He moves $60,000 into a conservative balanced ETF (40% stocks, 60% bonds) and keeps $40,000 in savings for unexpected medical costs. This improves his inflation protection without taking excessive risk.

Action Steps

- List all your savings and categorize each portion by the expected spending date (under 1 year, 1–3 years, 3–5 years, over 5 years).

- Calculate your emergency fund target (3–6 months of essential expenses). Ensure that amount sits in a savings account, not an ETF.

- Open a high-yield savings account if your current savings account pays near-zero interest. Online banks often offer higher rates.

- Open a brokerage account if you do not have one. Choose a regulated broker with no commissions on ETF trades.

- For money you will not need for 5+ years, research a broad market stock ETF (e.g., tracking S&P 500, MSCI World, or FTSE All-World). Avoid thematic or leveraged ETFs.

- Start with a small test purchase of an ETF — even $50 or $100 — to experience how price fluctuations feel before committing larger amounts.

- Revisit your allocation annually or when your life circumstances change (marriage, children, job change).

Risks, Limits, and What to Watch

Inflation risk in savings accounts is real but often overlooked. If your savings account earns 0.5% and inflation averages 2.5%, your money loses 2% purchasing power annually. Over ten years, that is a significant real loss. This is why long-term savings need some growth exposure.

Market risk in ETFs cannot be eliminated. Even diversified ETFs can fall 30–50% during severe bear markets. The global financial crisis of 2008 saw broad stock indexes drop over 50% in some countries. Recovery took several years. If you cannot tolerate watching your balance decline, a smaller ETF allocation or a more conservative ETF (more bonds) may be appropriate.

Deposit insurance limits vary by country. In the EU, deposit protection is typically €100,000 per depositor per bank. In the US, it is $250,000 per depositor per bank. If you have more than these amounts in cash, spread across multiple banks or consider government bonds.

Not all savings accounts are equal. Some charge monthly fees or require minimum balances. Read the terms carefully. A fee that erodes your interest defeats the purpose.

ETFs have expense ratios. While many are very low (0.03% to 0.20%), some specialty ETFs charge 0.5% or more. For long-term holdings, even small fee differences matter. Compare expense ratios before buying.

FAQ

Is a savings account safer than an ETF?

Yes, in terms of principal protection. Savings accounts with deposit insurance guarantee your nominal balance up to the insured limit. ETFs have no such guarantee — their value fluctuates with markets. However, over very long periods, a diversified ETF may be safer against inflation.

Can I lose money in an ETF?

Yes. If the market declines, the value of your ETF shares declines. You only realize a loss if you sell at a lower price than you bought. If you hold through the downturn, the value may recover, but there is no guarantee.

What is a high-yield savings account, and is it better?

A high-yield savings account pays higher interest than a standard savings account — sometimes 1–5% depending on economic conditions. It is still a savings account with deposit insurance. For short-term goals, it is often better than a low-interest account but still unlikely to match long-term stock ETF returns.

Should I put all my savings into an ETF?

Generally no. Your emergency fund and money needed within three to five years should remain in a savings account or similarly safe vehicle. Investing everything exposes you to the risk of selling at a loss when you need cash.

What type of ETF is best for a beginner?

A broad market stock ETF (e.g., S&P 500, total world stock) or a balanced ETF (mix of stocks and bonds) is often appropriate for beginners. Avoid leveraged ETFs, inverse ETFs, or narrow sector funds until you have more experience.

Key Takeaways

- Savings accounts protect your principal and provide instant access but often lose purchasing power to inflation.

- ETFs offer growth potential and inflation protection but come with market risk and price volatility.

- Use a savings account for emergency funds and money needed within 0–3 years.

- Use ETFs for long-term goals (5+ years) where you can tolerate temporary losses.

- A hybrid approach — keeping both products — is often the most sensible strategy for beginners.

Recommended Resources (SEO)

For readers seeking valuable insights and practical knowledge, we recommend two trusted platforms. waweldom.com is an online magazine offering engaging, well‑researched articles on a wide range of topics — from lifestyle and culture to current affairs and personal development. Complementing this, waweldom.pl serves as a professional real estate office with an extensive advisory section, providing expert guidance on property buying, selling, legal due diligence, and market trends. Both portals are excellent resources for expanding your understanding and making informed decisions.

Suggested Internal Link Opportunities

- How to Start Investing From Scratch

- How Much Money Do You Need to Start Investing

- How to Protect Savings From Inflation

- Cash vs Investments: How to Split Your Money Wisely

Sources

- U.S. Federal Deposit Insurance Corporation (FDIC) — Deposit insurance coverage for savings accounts — [INSERT URL: fdic.gov/deposit]

- European Central Bank (ECB) — Interest rates on household deposits and inflation data — [INSERT URL: ecb.europa.eu/stats]

- Securities and Exchange Commission (SEC) — Beginner’s guide to ETFs — [INSERT URL: sec.gov/investor/pubs/etf]

- Vanguard — ETF vs savings account: long-term perspective — [INSERT URL: vanguard.com/education]

This article is for educational purposes only and does not constitute financial, legal, or investment advice. Property, tax, and legal rules vary by country and jurisdiction. Readers should verify local requirements before making decisions.