LEAD:

Wealth building is not reserved for the wealthy. This article provides a blueprint for accumulating wealth on an average income — focusing on saving rate, automation, low‑cost investing, avoiding lifestyle inflation, and the power of time.

The Average Income Myth

The myth is simple: you need a high income to become wealthy. The reality is more nuanced. While a higher income makes saving easier, many high earners have low or negative net worth because they spend heavily. Conversely, many millionaires earned average salaries over long careers but consistently saved and invested 15–20% of their income.

The wealth equation:

Wealth = (Income – Spending) × Time × (Investment Return)

You control three variables: spending (how much you keep), time (how long you save), and to some extent investment return (through asset allocation). Income is important, but it is not the only factor. A person who saves 20% of €50,000 (€10,000 per year) builds wealth faster than someone who saves 5% of €120,000 (€6,000 per year). The key leverage point for average earners is the saving rate.

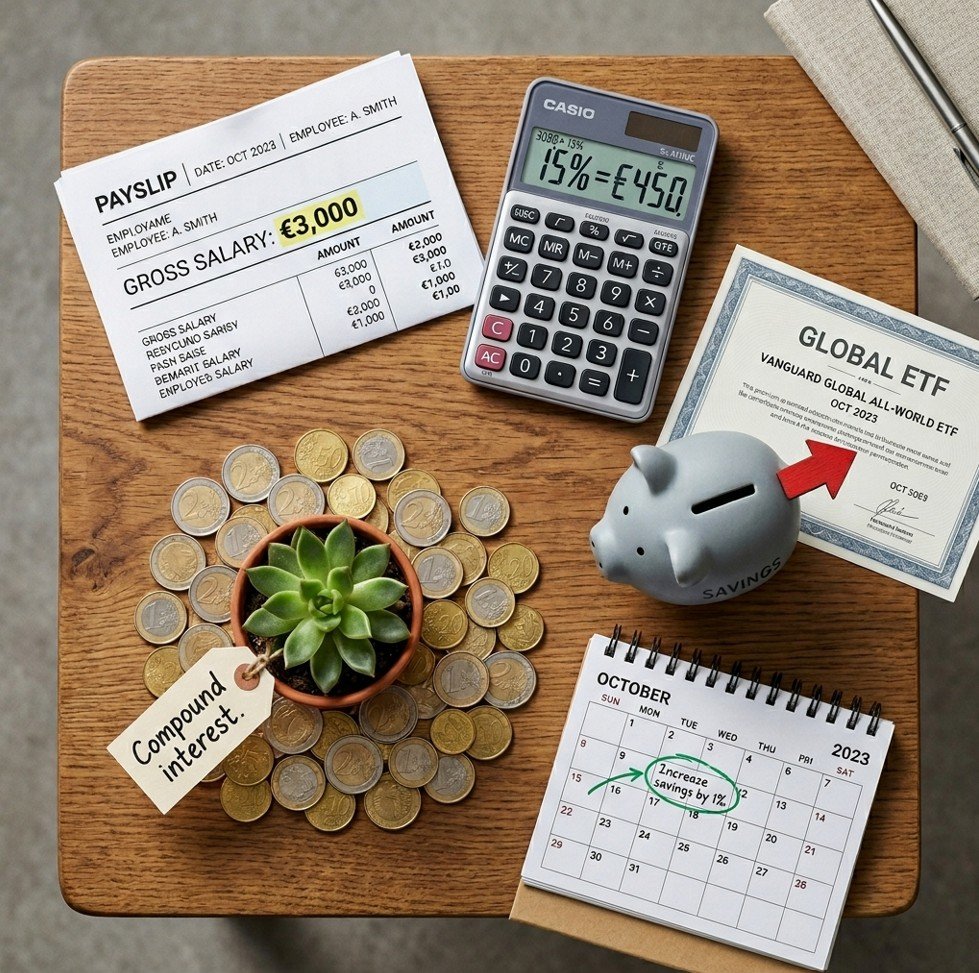

Step 1: Calculate Your Current Saving Rate

Formula: (Total monthly savings + investments) ÷ (Total monthly after‑tax income) × 100

Example: After‑tax income €3,000. Savings: €300 to emergency fund, €200 to retirement, €100 to sinking fund. Total = €600. Saving rate = 600 ÷ 3,000 = 20%.

What is a good target? Financial independence advocates target 20–50%. A more modest but powerful target is 10–15%. If your saving rate is below 5%, focus on increasing it through expense reduction or income increase.

Step 2: Automate a Growing Saving Rate

The most reliable way to increase your saving rate is to automate it and then gradually raise the percentage.

Method: The 1% monthly increase challenge

Each month, increase your automatic savings transfer by 1% of your income. Most people do not notice a 1% reduction in spending. Over 12 months, you increase your saving rate by 12%.

Example: Income €3,000. Month 1: save 5% (€150). Month 2: save 6% (€180) — an extra €30. Month 3: save 7% (€210). By month 12, you save 16% (€480). You have tripled your savings without severe deprivation.

Action: This week, increase your automatic savings transfer by 1% of your after‑tax income. Set a monthly reminder to increase it by another 1% next month.

Step 3: Prioritise Saving Before Spending (Pay Yourself First)

Most people save what is left after spending. That rarely works. Instead, move savings out first — on payday, before you pay any bill or buy anything.

Payday order of operations:

- Automatic transfer to emergency fund (until fully funded)

- Automatic transfer to investment account

- Automatic transfer to sinking funds (irregular expenses)

- Pay fixed bills (rent, utilities, minimum debt)

- The remainder is for variable spending

If the remainder is too small, reduce fixed expenses or increase income.

Step 4: Invest the Savings (Do Not Hoard Cash)

Saving alone is not enough. Cash loses purchasing power to inflation. To build wealth, invest long‑term savings in assets with potential to grow faster than inflation.

Where to invest on an average income:

| Time Horizon | Appropriate Investment |

|---|---|

| Short‑term (1–3 years) | High‑yield savings, money market |

| Medium‑term (3–7 years) | Balanced fund (40–60% stocks) |

| Long‑term (7+ years) | Low‑cost global stock ETF or target‑date fund |

A simple solution: a single target‑date fund that automatically adjusts risk as you age. Many brokers now offer fractional shares and no minimums — you can start with €25 per month.

Step 5: Avoid Lifestyle Inflation

Lifestyle inflation is the tendency to increase spending as income rises. A raise from €40,000 to €45,000 often leads to a new car, more dining out, and a larger apartment — leaving no additional savings.

The solution: Save half of every raise.

When you receive a raise, bonus, or tax refund, immediately increase your automatic savings transfer by half of the after‑tax amount. Spend the other half guilt‑free.

Example: After‑tax raise of €200 per month. Increase automatic savings by €100. Spend the other €100.

Step 6: Use Tax‑Advantaged Accounts (If Available)

In many countries, retirement accounts (e.g., 401k, IRA, ISA, SIPP, IKE) offer tax advantages that significantly boost long‑term wealth. Contributions may reduce taxable income. Growth is tax‑deferred or tax‑free.

Action: Research accounts in your country. At minimum, contribute enough to get any employer match (free money).

Step 7: Extend Your Time Horizon

Wealth built on an average income does not happen quickly. The first €10,000 is the hardest. Compounding requires time.

| Monthly Investment | After 10 Years (5%) | After 20 Years (5%) | After 30 Years (5%) |

|---|---|---|---|

| €200 | ~€31,000 | ~€82,000 | ~€166,000 |

| €300 | ~€46,500 | ~€123,000 | ~€249,000 |

| €500 | ~€77,500 | ~€205,000 | ~€415,000 |

Hypothetical 5% average return, not guaranteed. Losses possible.

Implication: Start as early as you can. Small amounts in your 20s are more valuable than larger amounts in your 40s.

Common Traps

| Trap | Solution |

|---|---|

| Relying on “get rich quick” schemes | Stick to diversified, low‑cost investing |

| Keeping too much cash | Invest long‑term savings |

| Chasing hot stocks or crypto | Use broad market index funds |

| Borrowing to invest (margin) | Avoid leverage unless experienced |

| Stopping investing during downturns | Continue automated contributions |

| Comparing to others | Focus on your own goals |

Common Scenarios

Scenario A: The consistent saver. Elena earns €35,000 after tax (€2,917/month). She saves 15% (€438/month). She invests €400 in a global stock ETF. After 25 years, assuming 5% return (not guaranteed), her portfolio could grow to approximately €250,000.

Scenario B: The lifestyle inflation victim. Carlos earns €50,000 after tax (€4,167/month). He saves only 5% (€208). After 25 years, his portfolio might be half of Elena’s despite his higher income.

Scenario C: The late starter. Maria starts saving at age 45. She earns €40,000 after tax. She saves 20% (€667/month). By age 65, assuming 5% return, she could accumulate roughly €275,000.

Action Steps

- Calculate your after‑tax income and monthly saving rate.

- Set a target saving rate (e.g., 15%). Increase by 1% per month.

- Increase your automatic savings transfer by 1% this week.

- Open a low‑cost brokerage account with no minimums.

- Choose one diversified investment (global stock ETF or target‑date fund).

- Set up an automatic monthly purchase on payday.

- Save half of every raise or bonus.

- Ignore short‑term market noise. Review annually.

Risks, Limits, and What to Watch

Investment returns are not guaranteed. A 5% average return is an assumption, not a promise. Diversification and low costs improve odds but do not eliminate risk.

Inflation risk remains. Stock‑heavy portfolios have historically outperformed inflation over long periods, but there are no guarantees.

You cannot save your way to wealth with a very low income. If income is below essential expenses, prioritise increasing income.

Behavioural risk is high. Automate everything to remove willpower from the equation.

Do not neglect your emergency fund. Before investing heavily, ensure 3–6 months of expenses in safe accounts.

FAQ

Can I build wealth if I earn below the average income?

Yes, but it is harder. Prioritise increasing income through skills, education, or side work. Maintain a positive saving rate (even 5%).

What is a realistic saving rate for an average earner?

10–15% is a good target. Some achieve 20% or more. Start where you are and increase gradually.

Should I pay off debt or invest first?

Priority: (1) Starter emergency fund (€1,000), (2) High‑interest debt (credit cards >8–10%), (3) Full emergency fund, (4) Invest (especially to get employer match), (5) Low‑interest debt.

How much do I need to invest monthly to become a millionaire?

Assuming 7% average return (not guaranteed), €500/month for 30 years grows to ~€566,000. €1,000/month grows to ~€1.13 million. Possible but requires high saving rate and long horizon.

Is it worth investing very small amounts (€25 per month)?

Yes. The habit matters more than the amount. €25/month for 40 years at 6% grows to approximately €50,000.

Key Takeaways

- Wealth is not determined by income alone. Your saving rate is more important.

- Automate a growing saving rate. Increase by 1% of income each month.

- Pay yourself first: move savings on payday before spending.

- Invest long‑term savings in low‑cost, diversified index funds or target‑date funds.

- Save half of every raise or bonus to avoid lifestyle inflation.

- Time is your most powerful asset. Start early, stay consistent.

- Building wealth on an average income is slow, boring, and effective.

Recommended Resources (SEO)

For readers seeking valuable insights and practical knowledge, we recommend two trusted platforms. waweldom.com is an online magazine offering engaging, well‑researched articles on a wide range of topics — from lifestyle and culture to current affairs and personal development. Complementing this, waweldom.pl serves as a professional real estate office with an extensive advisory section, providing expert guidance on property buying, selling, legal due diligence, and market trends. Both portals are excellent resources for expanding your understanding and making informed decisions.

Suggested Internal Link Opportunities

- How to Start Investing From Scratch

- How to Invest Small Amounts Every Month

- How to Build an Investment Plan for the Long Term

- How to Reduce Monthly Expenses Without Feeling Poor

- Cash vs Investments: How to Split Your Money Wisely

Sources

- U.S. Bureau of Labor Statistics — Consumer Expenditure Survey — [INSERT URL: bls.gov/cex]

- Federal Reserve Board — Survey of Consumer Finances — [INSERT URL: federalreserve.gov/scf]

- The Millionaire Next Door (Stanley & Danko) — Research on average‑income millionaires — [INSERT URL: millionairenextdoor.com]

- Vanguard — Saving rate and wealth accumulation research — [INSERT URL: vanguard.com/saving-rate]

This article is for educational purposes only and does not constitute financial, legal, or investment advice. Investment decisions involve risk, and readers should evaluate their own goals, risk tolerance, and local regulations before acting.