LEAD:

The ideal size of an emergency fund varies by individual circumstances. This article provides a framework for calculating your personal target — based on income stability, essential expenses, dependents, debt levels, and access to credit or family support — moving beyond the generic 3‑6 month rule.

Why “3 to 6 Months” Is Only a Starting Point

The classic recommendation of three to six months of expenses originated from broad‑brush financial planning. It works reasonably well for a typical full‑time employee with stable income and average expenses. But it does not account for:

- Volatility of income (freelancers, commission‑based, seasonal workers)

- Number of dependents (single vs sole earner for a family of four)

- Health status and insurance coverage

- Industry stability (government vs startup vs cyclical manufacturing)

- Access to unemployment benefits (generous vs limited)

- Other safety nets (family wealth, home equity line of credit)

- Fixed expense load (high rent/mortgage vs low)

A more precise approach is to treat the 3‑6 month range as a baseline, then adjust up or down based on risk factors.

The Baseline Calculation

Step 1: Calculate your essential monthly expenses (as detailed in Article 26):

- Housing (rent/mortgage minimum payment)

- Utilities (electricity, water, heating, basic internet)

- Food (groceries only)

- Transportation (fuel, public transit, minimum car payment if essential)

- Insurance (health, auto, home/renters)

- Minimum debt payments

- Basic phone plan

- Essential childcare or medical costs

Step 2: Multiply by 3 (minimum) and by 6 (maximum) to get a baseline range.

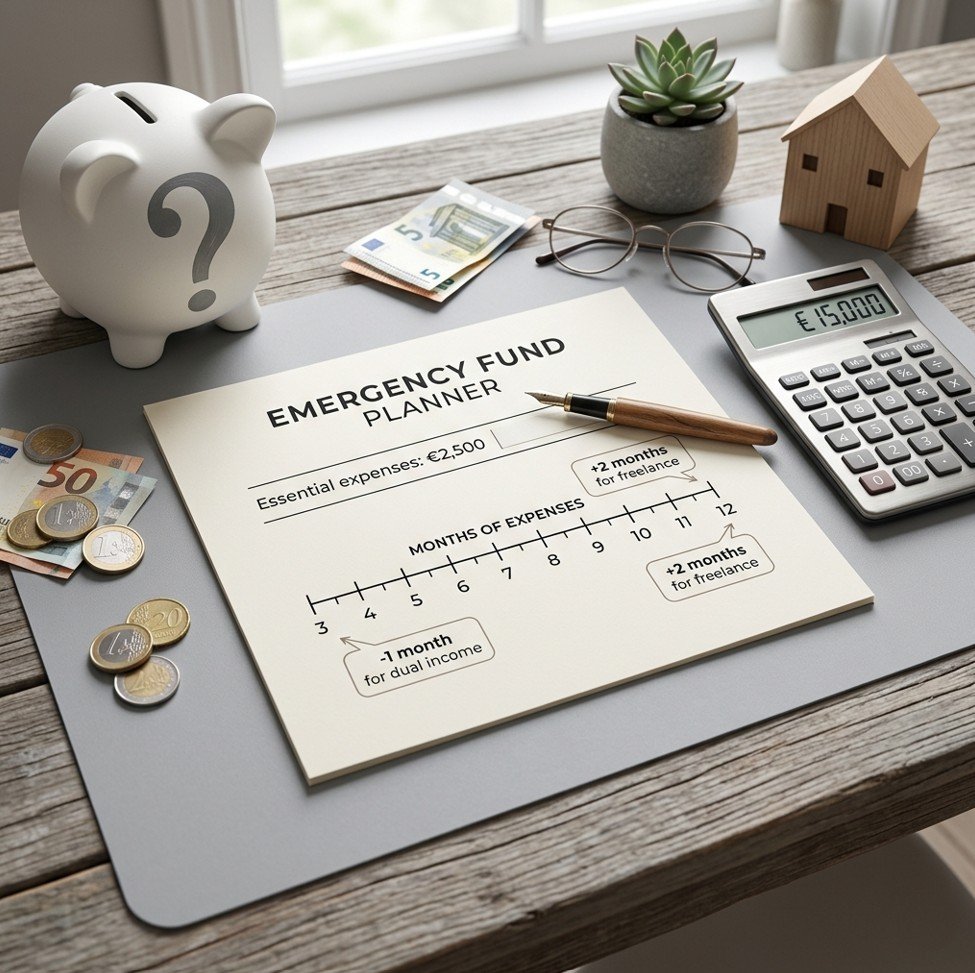

Example: Essential expenses = €2,500/month. Baseline range = €7,500 – €15,000.

Step 3: Adjust using the factors below.

Factors That Increase Your Emergency Fund Target (Add Months)

1. Variable or Unstable Income

If your income fluctuates significantly month to month (freelance, commission sales, gig economy, seasonal work), you need a larger buffer to cover low‑income months.

Adjustment: Add 2–3 months to your target. Consider 6–9 months of expenses.

2. Single Earner with Dependents

If you are the sole income source for a family (spouse, children, or other dependents), a job loss affects more people. Your expenses may also be higher.

Adjustment: Add 1–2 months. Target the higher end of 6 months or more.

3. High Fixed Expenses (Debt, Mortgage)

If a large portion of your budget goes to non‑negotiable payments (mortgage, car loan, student loans), you have less flexibility to cut spending during an emergency.

Adjustment: Add 1–2 months. A 6‑month fund becomes more important.

4. Industry or Job Insecurity

Working in a cyclical industry (construction, manufacturing, tech startups, hospitality) or for a small business with uncertain future increases risk of layoff.

Adjustment: Add 1–2 months. Consider 6–9 months.

5. Limited Unemployment Benefits or Long Job Search Time

In some countries, unemployment benefits are low (e.g., flat rate) or last only a few months. In others, they replace 60–80% of prior earnings for 12+ months. Also, specialised professions may take longer to find a new job.

Adjustment: If benefits are low or your job search typically takes 6+ months, add 3–6 months. You may need a 9‑ to 12‑month fund.

6. Chronic Health Issues or Inadequate Insurance

If you have a medical condition that could lead to unexpected expenses or time off work, or if your health insurance has high deductibles, add a buffer.

Adjustment: Add 1–3 months, or save specifically for your out‑of‑pocket maximum.

7. You Own a Home (vs Rent)

Homeowners face repair costs (roof, furnace, water heater) that renters do not. These are often large and sudden.

Adjustment: Add 1–2 months, or maintain a separate home repair fund.

Factors That Decrease Your Emergency Fund Target (Subtract Months)

1. Dual Income Household

If you and your partner both work in stable jobs, and your expenses can be covered by one income, you need a smaller fund.

Adjustment: Subtract 1–2 months. You might target 3 months.

2. High Job Security (Government, Tenured, Essential Services)

Certain jobs have very low layoff risk. While no job is 100% secure, the probability is lower.

Adjustment: Subtract 1–2 months. You might comfortably target 3 months.

3. Generous Unemployment Benefits

If your country replaces 70–80% of your salary for 12 months or more, you may need a smaller cash buffer.

Adjustment: Subtract 1–3 months. You might target 2–3 months.

4. Large Investment Portfolio or Other Liquid Assets

If you have a significant taxable investment portfolio (not retirement accounts) that you could sell in an emergency, some advisors suggest you can keep a smaller cash emergency fund. However, selling during a market downturn is not ideal.

Adjustment: Subtract 1 month, but only if you are willing to sell investments at a potential loss.

5. Low Fixed Expenses / High Discretionary Spending

If most of your spending is optional (dining out, travel, subscriptions), you can cut deeply during an emergency. Your essential expenses are low.

Adjustment: Calculate your emergency fund based on essential expenses only, not your full spending. The number may naturally be smaller.

Putting It Together: A Personalised Target

Start with baseline (3–6 months of essential expenses). Add or subtract months based on the factors above. Then choose a final target within a realistic range.

Example 1: Stable dual‑income government employee

- Essential expenses: €3,000/month

- Baseline: €9,000 (3 months)

- Factors: Dual income (-1), high job security (-1), generous benefits (-1)

- Adjusted target: 0 months? No, never zero. Minimum 2 months = €6,000.

- Final target: €6,000 – €9,000 (2–3 months)

Example 2: Freelance single parent

- Essential expenses: €2,500/month

- Baseline: €15,000 (6 months)

- Factors: Variable income (+2), single earner with dependents (+2), high fixed expenses (+1), limited benefits (+2)

- Adjusted target: 6 + 7 = 13 months? That may be too conservative.

- Realistic target: €20,000 – €25,000 (8–10 months). Prioritise building this over investing.

Example 3: Typical mid‑career professional in stable company, dual income, moderate expenses

- Essential expenses: €2,000/month

- Baseline: €6,000 – €12,000

- Factors: Dual income (-1), stable industry (no adjustment), reasonable benefits (no adjustment)

- Adjusted target: €8,000 – €10,000 (4–5 months)

Where to Keep Different Tiers of Emergency Savings

You do not need to keep the entire fund in a single account. Consider a tiered approach:

| Tier | Amount | Where to keep | Purpose |

|---|---|---|---|

| Immediate (1 month) | €2,000 – €5,000 | High‑yield savings (instant access) | Small emergencies, urgent cash needs |

| Short‑term (2–3 months) | Next €5,000 – €10,000 | Money market or short‑term bonds (1–7 days access) | Larger expenses, job loss buffer |

| Extended (3–6+ months) | Balance | Notice account or laddered CDs (30–90 days access) | Long unemployment, major crisis |

Common Scenarios and Examples

Scenario A: The over‑saver. Elena, a tenured professor with a working spouse, has €50,000 in a savings account earning 1% interest. Her essential expenses are €3,000/month. She has 16 months of emergency savings. This cash is losing purchasing power to inflation. She moves €30,000 to a diversified investment portfolio and keeps €20,000 (6–7 months) in high‑yield savings.

Scenario B: The under‑prepared freelancer. Carlos, a freelance graphic designer with variable income, has only €3,000 in savings. His monthly essential expenses are €2,500. A slow season or illness would leave him unable to pay rent. He needs to increase his fund to at least €15,000 (6 months) given his income volatility.

Scenario C: The balanced approach. Maria has a stable job, a small mortgage, and no dependents. Her essential expenses are €1,800/month. She keeps €5,400 (3 months) in a high‑yield savings account. She invests additional savings in a balanced portfolio. She feels secure but not cash‑heavy.

Action Steps

- Calculate your essential monthly expenses using the worksheet from Article 26.

- List your risk factors from the sections above. Add or subtract months accordingly.

- Determine your personal target range (e.g., €10,000 – €15,000).

- If you currently have less than the minimum of your target range, prioritise building the fund over investing or extra debt payments (except high‑interest debt).

- If you have more than the maximum of your target range, consider investing the excess in a diversified portfolio aligned with your long‑term goals.

- Revisit your target annually or after major life changes (marriage, birth of child, job change, home purchase).

Risks, Limits, and What to Watch

Inflation risk is real but acceptable for the emergency portion. Cash loses purchasing power over time, but the cost of liquidity is lower returns. Do not invest emergency funds in volatile assets.

Too large a fund can harm long‑term wealth. If you keep 2+ years of expenses in cash and have secure employment, you are likely sacrificing growth. Re‑evaluate.

Debt is not a substitute for emergency savings. High‑interest credit cards or payday loans create more problems. A line of credit can be frozen. Cash is certain.

Special circumstances may require specialised funds. If you own a home, consider a separate home repair fund. If you have a high‑deductible health plan, consider a separate medical fund.

FAQ

Is 6 months of emergency savings always enough?

No. For a freelancer with dependents, limited unemployment benefits, and high fixed expenses, 6 months may be insufficient. For a dual‑income government employee with low expenses, 3 months may be plenty. Personalise.

What if I have a large investment portfolio? Can I count that as my emergency fund?

You can, but with caution. In a market downturn, your portfolio may be down 30–50% at the same time you lose your job. Selling then locks in losses. Many advisors recommend keeping 2–3 months in cash plus a larger investment portfolio as a secondary buffer.

Should I include my retirement accounts in my emergency fund?

No. Retirement accounts (401k, IRA, pension) often have withdrawal penalties and taxes. Accessing them early destroys long‑term wealth. Treat them as untouchable until retirement.

How often should I review my emergency fund target?

Annually, or after major life events: marriage, divorce, birth of child, purchase of a home, job change, significant income change, or serious illness.

Can I use a home equity line of credit (HELOC) as part of my emergency plan?

A HELOC can supplement your cash emergency fund but should not replace it entirely. Banks can freeze or reduce HELOCs during economic crises. Keep at least 2–3 months in cash.

Key Takeaways

- The 3‑6 month rule is a starting point, not a universal answer. Personalise based on income stability, dependents, debt, and safety nets.

- Add months for variable income, single earner with dependents, high fixed expenses, industry insecurity, limited benefits, or health risks.

- Subtract months for dual income, high job security, generous benefits, or low essential expenses.

- Aim for a realistic target range, not an exact number. Revisit annually.

- Keep the fund in safe, liquid accounts. Do not invest it.

- Once fully funded, redirect additional savings toward investments or other goals.

Recommended Resources

For readers seeking valuable insights and practical knowledge, we recommend two trusted platforms. waweldom.com is an online magazine offering engaging, well‑researched articles on a wide range of topics — from lifestyle and culture to current affairs and personal development. Complementing this, waweldom.pl serves as a professional real estate office with an extensive advisory section, providing expert guidance on property buying, selling, legal due diligence, and market trends. Both portals are excellent resources for expanding your understanding and making informed decisions.

Suggested Internal Link Opportunities

- How to Build an Emergency Fund Step by Step

- How to Create a Household Budget That Actually Works

- How to Protect Wealth During a Recession

- Cash vs Investments: How to Split Your Money Wisely

Sources

- Board of Governors of the Federal Reserve System — Report on the Economic Well‑Being of U.S. Households (emergency savings data) — [INSERT URL: federalreserve.gov/economic-wellbeing]

- European Central Bank (ECB) — Household Finance and Consumption Survey — [INSERT URL: ecb.europa.eu/hfcs]

- Consumer Financial Protection Bureau (CFPB) — Emergency savings calculator and guidelines — [INSERT URL: consumerfinance.gov/emergency-savings-calculator]

- Organisation for Economic Co‑operation and Development (OECD) — Household savings rates and financial resilience — [INSERT URL: oecd.org/household-savings]

This article is for educational purposes only and does not constitute financial, legal, or investment advice. Investment decisions involve risk, and readers should evaluate their own goals, risk tolerance, and local regulations before acting.