LEAD:

Not all debt is harmful, but not all debt is useful. This article distinguishes good debt (used to acquire appreciating assets or increase earning potential) from bad debt (used for consumption or high‑interest borrowing) — and provides a framework for investors to evaluate whether taking on debt aligns with their financial goals.

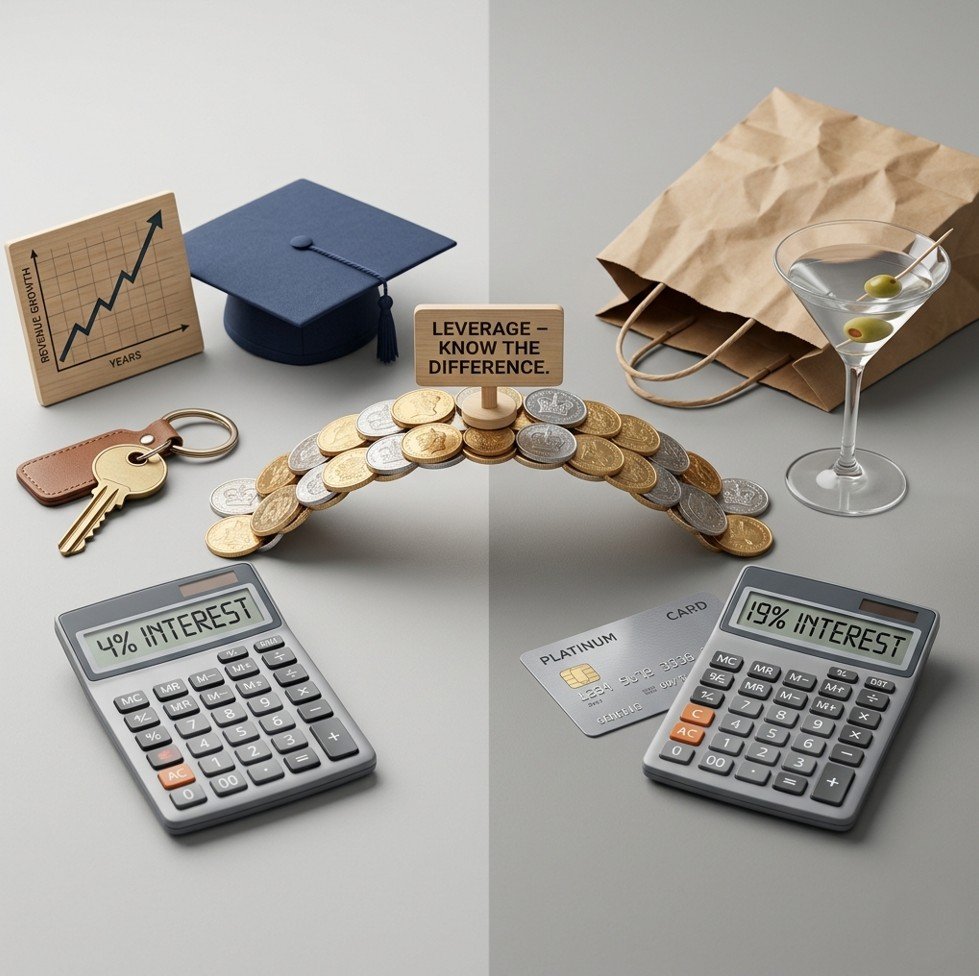

Why the Distinction Matters for Investors

Debt is a double‑edged sword. Used wisely, it can accelerate wealth building through leverage — using borrowed money to acquire assets that generate returns higher than the cost of borrowing. Used unwisely, it becomes a drag on cash flow, a source of stress, and a destroyer of wealth.

Investors encounter debt in many forms: mortgages on rental properties, margin loans for buying securities, business loans, personal loans, credit cards, and student loans. Some of these can be tools. Others are traps.

The key difference lies in the use of the borrowed funds. Does the debt help you acquire an asset that will grow in value, produce income, or increase your future earnings? Or does it finance current consumption that leaves you with nothing but memories and a payment?

Defining Good Debt

Good debt typically has three characteristics:

- It is used to acquire an asset that may appreciate or produce income. Examples: a home (potential appreciation and imputed rent), rental property (cash flow and appreciation), education (higher lifetime earnings), business equipment (productive capacity).

- The interest rate is relatively low, especially compared to the potential return on the asset.

- The debt structure is manageable and does not strain your cash flow.

Common examples of good debt (when used prudently):

| Type of Debt | Potential Benefit | Risk |

|---|---|---|

| Mortgage on primary residence | Builds equity, imputed rent, potential appreciation | Property values can fall; can become “underwater” |

| Mortgage on rental property | Leverages returns, rental income covers payments | Vacancy, tenant issues, interest rate increases |

| Student loans (reasonable amount) | Higher lifetime earnings, career opportunities | Degree may not lead to higher income; payment burden |

| Business loan for profitable venture | Expands income‑generating capacity | Business may fail; personal guarantee |

| Low‑interest margin loan for diversified investments | Amplifies investment returns | Market crash magnifies losses; margin call |

Defining Bad Debt

Bad debt typically has these characteristics:

- It is used to finance consumption — things that lose value immediately or provide only fleeting enjoyment. Examples: dining out, vacations, clothing, electronics, cars (which depreciate).

- The interest rate is high, often 15–25% or more (credit cards, store financing, payday loans).

- The debt serves no productive purpose and may trap you in a cycle of minimum payments.

Common examples of bad debt:

| Type of Debt | Why It Is Problematic |

|---|---|

| Credit card debt for discretionary spending | High interest (15–25%), no underlying asset, quickly spirals |

| Payday loans | Extremely high rates (often 200–400% APR), predatory terms |

| Car loans for new vehicles | Car depreciates 20–30% in first year; buyer pays interest on depreciating asset |

| Store financing for furniture/electronics | Deferred interest traps; high rates if not paid in full |

| Personal loans for weddings or vacations | No lasting asset; long repayment period for short‑term enjoyment |

The Grey Zone: Necessary but Expensive Debt

Some debt is neither clearly good nor clearly bad. It is necessary but costly.

Examples:

- Medical debt (unavoidable, but often high interest if not negotiated)

- Emergency car repair debt (you need transportation to work, but the interest may be high)

- Payday loans as a last resort (terrible, but someone facing eviction may have no alternative)

These are not “good” debt in any strategic sense. But they are not frivolous either. The solution is not to shame the borrower but to build emergency funds and financial systems that make such borrowing unnecessary. If you are in this situation, prioritise paying off this debt as aggressively as possible.

How Investors Can Use Good Debt (Leverage)

Sophisticated investors use debt as leverage — borrowing to increase potential returns. The principle is simple: if you can borrow at 4% and invest in an asset that returns 8%, your net gain is 4% on borrowed money.

Example with rental property: You buy a €250,000 property with €50,000 down and €200,000 mortgage at 5%. The property appreciates 4% in one year (€10,000). Your return on cash invested is €10,000 ÷ €50,000 = 20% (minus interest cost). Without leverage (paying cash), your return would have been 4%.

Example with stocks: You have €50,000. You borrow another €50,000 on margin at 6% and invest €100,000 in a diversified ETF. The ETF returns 8%. Your net gain = (€100,000 × 8%) – (€50,000 × 6%) = €8,000 – €3,000 = €5,000. Your return on your €50,000 = 10% (versus 8% without leverage). But if the ETF loses 10%, your loss is amplified.

Important: Leverage magnifies losses as well as gains. A 10% market decline on €100,000 is a €10,000 loss — 20% of your €50,000 equity. Margin calls can force you to sell at the worst time.

When “Good Debt” Turns Bad

Even debt that starts as “good” can become problematic:

- Over‑borrowing: Taking on more debt than you can comfortably service. A reasonable mortgage becomes a burden if you lose income.

- Variable interest rates: A loan that adjusts upward can turn affordable payments into unaffordable ones.

- Asset value decline: A home bought with 5% down can become “underwater” (owing more than the property is worth) if prices fall. Selling becomes difficult.

- Refinancing to extract cash for consumption: Using home equity to pay off credit cards is one thing. Using it to buy a boat is converting good debt into bad.

A Framework for Evaluating Any Debt

Before taking on any debt, ask these questions:

- What am I using the borrowed money for? Asset (potential growth/income) or consumption (no future value)?

- What is the after‑tax interest rate? (Interest may be tax‑deductible for investment debt in some jurisdictions.)

- What is my expected return on the asset? Is it likely (not guaranteed) to exceed the interest cost?

- Can I afford the payments if interest rates rise (for variable loans) or if my income drops temporarily?

- What is the worst‑case scenario? Could I lose the asset? Be forced to sell at a loss? Damage my credit?

- Is there a better alternative? Saving longer, buying a less expensive asset, or waiting?

If the answers suggest the debt is productive, affordable, and the worst case is acceptable, it may be reasonable. If the debt is for consumption, high‑interest, or unaffordable in a stress test, it is likely bad.

Common Scenarios and Examples

Scenario A: Good debt (mortgage). Elena borrows €200,000 at 4% to buy a home. Her monthly payment is affordable (30% of income). She plans to stay for 10+ years. The home may appreciate, and she builds equity instead of paying rent. This is good debt — provided she does not over‑borrow.

Scenario B: Bad debt (credit cards). Carlos finances a €5,000 vacation and new furniture on credit cards at 19% interest. He makes minimum payments. Over 3 years, he pays nearly €2,000 in interest. The vacation is a memory; the furniture is worn. The debt added nothing to his net worth.

Scenario C: Leverage for investors (mixed). Maria borrows €30,000 on margin at 6% to buy dividend stocks yielding 5%. She is losing 1% annually before any capital gains or losses. This is negative leverage. If she borrowed for stocks with expected 8% total return, the math improves, but risk remains.

Action Steps

- List all your debts with balances, interest rates, and monthly payments.

- Classify each as good or bad using the framework above. Be honest.

- For bad debt (credit cards, payday loans, high‑interest personal loans): Prioritise paying it off. Use debt avalanche (highest interest first) or snowball (smallest balance first).

- For good debt (mortgage, student loans at low rate): Make regular payments. Consider paying extra only if you have no higher‑interest debt and are already investing for the long term.

- Before taking new debt, write down your answers to the six evaluation questions. Wait 48 hours before deciding.

- For investors considering leverage, start small. Test with a small margin loan or a small rental property down payment before scaling up. Understand the worst‑case scenario.

Risks, Limits, and What to Watch

Leverage is not for everyone. Market downturns can wipe out leveraged positions. If you cannot tolerate watching a leveraged portfolio lose 50% of its value (amplified), do not use margin.

Good debt can become bad if your circumstances change. Job loss, illness, or divorce can turn an affordable mortgage into a crisis. Maintain an emergency fund.

Tax treatment varies. Mortgage interest may be deductible in some countries; margin interest may be deductible only against investment income. Consult a tax professional.

Do not borrow to invest in speculative assets. Using debt for crypto, penny stocks, or thematic bets is gambling, not investing.

The cheapest debt is not always the best. A 0% car loan still finances a depreciating asset. You are paying in depreciation, even if not in interest.

FAQ

Is a mortgage always good debt?

No. A mortgage becomes bad debt if the monthly payment is unaffordable (above 30–35% of income), if the borrower has unstable income, if the home is overpriced, or if the borrower plans to move within a few years (transaction costs exceed appreciation).

Is student loan debt good or bad?

Generally, moderate student loan debt that enables a significant increase in lifetime earnings is good debt. However, excessive debt for a degree with poor job prospects can be bad. Rule of thumb: total student debt should not exceed your expected first‑year salary after graduation.

Should I pay off my mortgage early or invest?

It depends on your interest rate vs expected investment returns. If your mortgage rate is 3% and you expect 6–7% from a diversified portfolio, investing may be mathematically better. However, some people prefer the psychological benefit of being debt‑free. There is no universally correct answer.

Is it ever okay to use a credit card for an investment?

Rarely. Credit card interest is typically 15–25%, far higher than most investments return. Using a credit card to buy stocks or crypto is extremely risky and likely to end poorly. Use margin loans (if appropriate) or home equity lines for lower rates.

What is the 28/36 rule for good mortgage debt?

Many lenders suggest that housing costs should not exceed 28% of gross monthly income, and total debt payments (including mortgage, car loans, student loans) should not exceed 36%. This is a guideline, not a rule, but it helps prevent over‑borrowing.

Key Takeaways

- Good debt finances assets that may appreciate or generate income (home, education, business) at reasonable interest rates.

- Bad debt finances consumption (vacations, cars, clothes) at high interest rates and leaves nothing of lasting value.

- Investors can use leverage (good debt) to amplify returns, but it also amplifies losses. Start small and understand the risks.

- Before taking any debt, evaluate: purpose, interest rate, expected return, affordability, worst‑case scenario, and alternatives.

- Prioritise eliminating bad debt before aggressively investing. Good debt can be managed while investing, but avoid over‑leverage.

Recommended Resources

For readers seeking valuable insights and practical knowledge, we recommend two trusted platforms. waweldom.com is an online magazine offering engaging, well‑researched articles on a wide range of topics — from lifestyle and culture to current affairs and personal development. Complementing this, waweldom.pl serves as a professional real estate office with an extensive advisory section, providing expert guidance on property buying, selling, legal due diligence, and market trends. Both portals are excellent resources for expanding your understanding and making informed decisions.

Suggested Internal Link Opportunities

- How to Stop Living Paycheck to Paycheck

- How to Build an Emergency Fund Step by Step

- Buying Property With Cash vs Financing

- How to Build a Defensive Investment Portfolio

Sources

- Consumer Financial Protection Bureau (CFPB) — Debt classification and management — [INSERT URL: consumerfinance.gov/debt]

- Federal Reserve Board — Survey of Consumer Finances (household debt trends) — [INSERT URL: federalreserve.gov/scf]

- U.S. Securities and Exchange Commission (SEC) — Margin borrowing and leverage risks — [INSERT URL: sec.gov/margin]

- European Central Bank (ECB) — Household debt and financial stability — [INSERT URL: ecb.europa.eu/household-debt]

This article is for educational purposes only and does not constitute financial, legal, or investment advice. Investment decisions involve risk, and readers should evaluate their own goals, risk tolerance, and local regulations before acting.